Two factors appear poised to positively affect the ability of households to purchase a home according to Fannie Mae's economists. In their initial 2016 Economic Developments commentary they see further labor market tightening and subsequent increases in compensation and job security. This, coupled with indications that lenders expect to continue to ease lending standards and expand mortgage access should help the housing recovery continue to expand.

Despite these positives however the economists see opposing factors pointing to constrained housing affordability, especially for first time homebuyers. These include continued strong home price appreciation outpacing income growth as well as rising mortgage interest rates.

In the past homebuyers have had some measures available to them, such as certain types of adjustable rate mortgages, to mitigate the impact of rising prices and rates but these are no longer widely available. Rising rents will also continue to affect affordability as they hamper renters' ability to save for a downpayment. They project the home sales market will continue to recover along with the broader economy in 2016 but that these affordability challenges will serve to moderate the pace.

They do see housing starts increasing this year compared to last because of lessening supply constraints and along with government spending and strong consumer spending, residential investment will help to drive economic growth. Overall they expect growth to accelerate slightly to 2.2 percent from an expected 2.0 percent in 2015.

Home building activity already showed some life in November with a surge in both single-family and multi-family housing starts and an increase in construction spending in the single-family sector. Existing homes sales dropped by double digits in November, falling to the lowest level since April 2014 but the report says implementation of the new TRID disclosure rule probably delayed some closings and may result in a higher volume of sales when December numbers come in next week.

New home sales increased in November but that report also downgraded earlier months' estimates. That put the three-month moving average well below the recent peak of earlier this year. The poor performance of November residential construction spending, combined with weak broker commissions implied by home sales, suggests much lower residential investment growth than predicted in Decembers forecast.

Leading indicators of home sales were mixed: The pending home sales index fell in November for the third time over the last four months, while purchase mortgage applications rebounded in November and rose further in December.

The increase in fed funds target rate at the December Federal Open Market Committee (FOMC) has so far had a minimal impact on mortgage rates. The economists say that the FOMC's dovish statement and minutes confirmed their expectations of a gradual pace of monetary policy normalization. They expect three fed funds rate hikes in 2016, one more than the fed funds futures market implies, but one less than the number indicated by the median projection of the FOMC members. Based on the strong December jobs report, muted inflationary pressures and a strong dollar Fannie Mae is looking for another hike in March and with current Fed guidance that the Fed will continue to reinvest its securities portfolio for at least another year.

The end results will be an increase in the 30-year fixed mortgage rate from 3.90 percent in the fourth quarter of 2015 to just 4.15 percent in the final quarter of 2016. Although they expect a gradual rise, a rate spike remains one of the downside risks for the housing market this year.

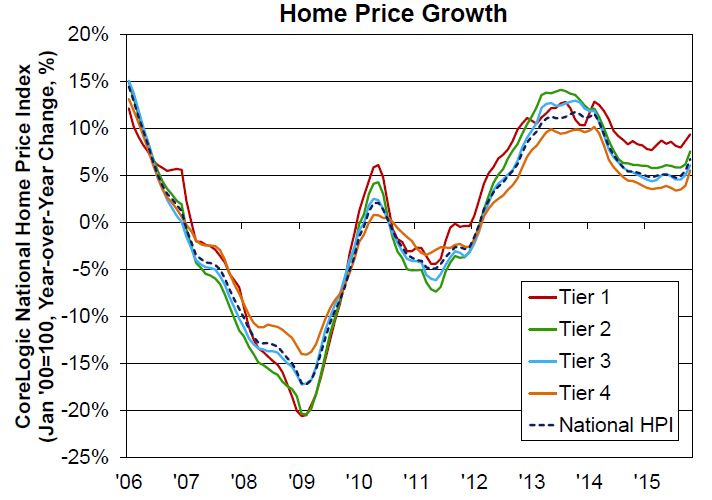

Home price appreciation remains strong. For example, the Case-Shiller national house price index rose 5.2 percent year over year in October and 6.3 percent in November each in sequence the largest increases since July 2014. In addition to the overall indices, CoreLogic provides trends of four individual home-price tiers calculated relative to the median national home price. The low-price tier has appreciated most rapidly in recent months, increasing 8.2 percent year over year in November. Of the four segments, this low-price tier is the only one with prices surpassing their pre-bubble peak. Most potential first-time homebuyers tend to focus on this segment of the market, where price gains continue to be robust and inventory is extremely lean so will likely encounter more difficulty in finding a home they can afford even with only gradual increases in mortgage rates.

Even with only gradual interest rate changes Fannie Mae's economists say they believe the home sales market "will face a challenge of deteriorating housing affordability, driven by continued strong home price appreciation that outpaces household income growth, especially for potential first-time homebuyers." Relatively tight lending standards will also contribute to moderate growth in home sales this year to about 4.0 percent compared to 6.0 percent in the year just ended. Multifamily housing starts have been very robust throughout the expansion, so only a small gain is expected this year given the already elevated levels.

The most upbeat projection in the report is that single family starts could rise about 17 percent this year compared to 9.0 percent in 2015, a number that came off of depressed levels. The caveat is that the prediction hinges on easing supply shortages (e.g., skilled labor, available lots) amid continued rising household formation. Nonetheless, inventory should still remain historically lean, leading to another year of solid price growth nationally although there will be significant variations across regions and especially in oil-producing states.